Social Mobilization and Institution Development for Urban Poor

SMID - Social Mobilization and Institution Development for Urban Poor

Social mobilization is the primary step of community development to organize and initiate action with their own enterprise and creativity. Through mobilization, people can organize themselves to take action collectively by developing their own plan and strategy for their socio-economic Development. TNULM envisages universal social mobilization of urban poor and vulnerable sections into Self Help Groups (SHGs) and their Federations. Generally, women from the poor and vulnerable households are mobilised as Self Help groups with a membership between 10 and 20.

TNULM lays particular emphasis on the mobilization of vulnerable sections of the urban poor population, such as SCs, STs, minorities, women-headed households, differently-abled, destitute, migrant labourers, and vulnerable occupational groups such as street vendors, rag pickers, domestic workers and construction workers etc.

Self Help Groups

Self Help Groups (SHGs) are groups of 10 to 20 women who come together to improve their living conditions by group savings and loans. These groups conduct regular meetings where the savings of the group is collected into a corpus fund, which is used to provide short-term loans to the members. After some time when the credit requirements of the members’ increase, the Self-Help Group may approach banks for loan.

As on 31st September, 2023, under TNULM, 1,38,536 SHGs have been formed in 649 ULBs and covering 15,42,487 members from Below Poverty Line HHs.

Special Self Help Groups

Organizing the vulnerable sections of the population into SHGs at the grass root level is the stepping-stone for their socio-economic development. Special Self Help Groups are being formed with differently-abled, transgenders, rag pickers or Nomadic tribes, widows, deserted women and the vulnerable people in urban areas. By networking as a group, these poor and vulnerable people can get a platform to voice their opinion and seek their entitlements. Formation of Special Self Help Groups plays an important role in inculcating the habit of creating micro savings, accessing micro loans and bank credit.

Under TNULM, so far 10,019 SHGs have been formed in 649 ULBs and covered 90,995 vulnerable members.

Categories of Special SHGs

| S.No | Types Of Special Group | No Of SHGs | No of Members Covered |

|---|---|---|---|

| 02 | Differently abled SHG | 1448 | 7964 |

| 03 | Sanitary worker SHG | 6452 | 67,746 |

| 04 | Transgender SHG | 254 | 1422 |

| 04 | Other vulnerable groups | 8723 | 69,784 |

| Total | 16,877 | 1,46,916 | |

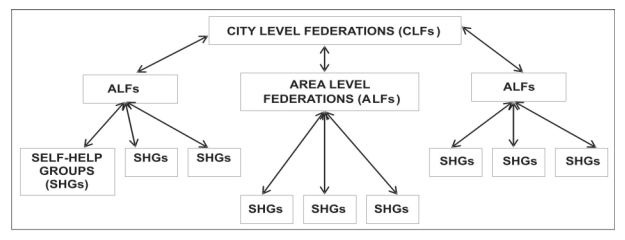

Area Level Federations

SHGs are founding blocks for collective action. However, they can’t achieve the larger purpose of addressing poverty and aiding economic and social development due to various limitations. The major limitations include limited scope for influence, limited bargaining power, low pool of human resources and capacities, limited capability of hiring support services. SHGs are federated at various levels to achieve economies of scale, which reduces transaction costs, sharing of resources, managing partnerships, self-regulation, sustainability, and sustainable collective action. Thus, the SHG federation is an association of primary organizations uniting for perceived common benefits.

Federations in NULM are formed at Area and City Levels to strengthen SHGs and to form new SHGs, monitor SHG activities including financial, address inter-SHG issues, Area-level Health, Nutrition and Sanitation issues, Skilling at Area level, building pool of such skilled individuals for citizen referral, provide information on livelihoods, etc. and represent the area or city in various forums.

Area Level Federation (ALF) is an association of SHGs consisting of representatives from all member SHGs, with the objective of supporting member-SHGs. The federation of SHGs is essential to deal with higher-level issues like bank-linkage (including bulk loan), inter-group lending, and negotiations with higher-level structures and to gain greater bargaining power over the rights and privileges of SHGs.

Responsibilities of an ALF

- Facilitate bank linkages for member SHGs i.e. opening of their accounts and helping them getting loans.

- Providing hand-holding support in the development of loan proposals and other documentation.

- Capacity building of SHGs.

- Facilitate member SHGs’ to get the benefits under NULM as well as access to social assistance benefits under various other Government programmes.

- Support the formation of new SHGs and monitor and evaluate functioning of its member SHGs.

- Resolve issues raised by member SHGs in accessing credit from banks.

- Raise issues of importance at the level of the City-Level Federations (CLFs).

- Regularly report to the ULB about the SHG’s functioning.

Registration of ALF:

Formation of ALFs:

- Minimum 10 -20 SHGs federated to ALF in all ULBs

- Paid the prescribed admission fee and the fixed annual subscription

- Each member SHG will elect one or two of its members to represent the group in the Executive Committee of the Federation for two years term

- An Executive Committee (EC) comprise minimum 11 member elected from General body meeting with representation of member SHG

- From the EC, four members have to be selected as the Office bearers

Training to ALF - Capacity Building:

ALF Executive members have to be trained about the roles and responsibilities, Governance and Accountability, financial literacy and procedures of Societies Act and periodical refresher trainings to all Executive Committee (EC) members. TNULM is empowering the ALFs by giving training for effective functioning of ALF members are given awareness among the participants about formation of SHG federations and their role, importance of SHG federations in institution building in future course.

ALF Office Bearer Training:

ALF Executive committee member training:

The Area level federation consists of minimum 11 to maximum of 21 members based on the SHG affiliation. Each ALF has 3 Sub-committees on Financial Inclusion, Livelihood and Social security. Each sub-committee has three to five members out of which, two are selected from among the Executive Committee and three are selected from General Body. The EC members are imparted training about their roles and responsibilities in ALF EC members training programme.

Under TNULM, so far 2975 ALFs have been formed and training imparted to 9188 ALF office bearers and EC members training completed at the cost of Rs 1.74 crore

Table 1. Bulk loan received by ALFs for 2020-2021 Kadambari ALF, Arupukottai – In all table same format

So far, 2975 ALFs have been formed with 51,329 SHGs consisting of 5,90,284 SHG members. Efforts are on to federate the remaining SHGs either into existing ALFs or by forming new ALFs.

Bulk loan to ALFs:

The primary objective of the ALF is to provide financial and non-financial support to member SHGs, thereby ensuring sustainability of the SHG movement. Financial intermediation by ALF has become very essential to minimize the impact of micro finance institutions who usually charge exploitative rates of interest.

Studies undertaken by TNULM have revealed that the entire financial requirement of the SHG members, particularly seasonal and special credit requirement, are not being fully met through internal lending or SHG bank linkage. In order to bridge the gap and support its members, ALFs are encouraged to take up financial intermediary role by availing bulk loan from banks. ALF Bulk loan will result in financial empowerment of the community-based organizations which will bring in sustainability in SHG movement.

Bulk Loans to ALFs offer significant advantages such as lower transaction costs, simple documentation procedures, easier supervision, targeted credit delivery, better quality of lending and better repayment through effective peer pressure.

With the approval of Government of Tamil Nadu, ALFs have been empowered to avail loan from Banks and lend to SHGs for gap filling required for financing and safe guard them from falling prey under the clutches of money lenders and other costly loan options for their short-term loans/ working capital requirements at an exorbitant interest rate.

For financial year, 2021-22 the various banks have lent bulk loan to 6 ALFs to the tune of Rs.1.96 crore. The ALFs facilitated the micro enterprises run by ALFs/ SHGs and motivate them to undertake profitable economic activities. Despite the fact that ALFs availing bulk loans are not eligible to receive Interest Subvention from DAY-NULM scheme, the District Mission Management Units in Tamil Nadu have always strived to set an example to the nation in facilitating higher levels of credit linkage through bulk loans in urban areas. The state Mission has also written to the National Mission to consider release of Interest subvention to ALFs availing Bulk Loans.

Table 1. Bulk loan received by ALFs for 2020-2021

| S.No | Name of the District | Name of the ALF | Amount of Bulk loan (Rs .Lakhs) | No of SHG benefited | No of LH activities supported through Bulk loan |

|---|---|---|---|---|---|

| 1 | Cuddalore | Malumiyarpettai ALF | 42 | 12 | 100 |

| 2 | Virudhungar | Kadambari ALF. Arupukottai | 16.69 | 9 | 114 |

| Adharsana ALF Chettiarpatty | 20.00 | 10 | 112 | ||

| 3 | Madurai | Pothugai ALF ,Balamedu | 39.05 | 9 | 92 |

| Karmugil ALF, Paravai | 19.05 | 4 | 46 | ||

| 4 | Tirunelveli | Jansi Rani ALF | 60 | 6 | 70 |

| Total | 196.79 | 50 | 534 | ||

Thus far, 2975 ALFs have been formed with 51,329 SHGs and consisting of 5,90,284 SHG members. Efforts are on to federate the remaining SHGs either into existing ALFs or by forming newer ALFs.

City Level Federations

- Strengthening of CBOs like SHGs, ALF and CLC in urban area

- Capacity building of CBOs about the scheme’s sensitization, awareness creation and capacity building training

- Resource mobilization and revenue generation for institutional sustenance and sustainability

- Facilitate the livelihood promotion through CBOs like, SHGs ALF and CLC through Bank Linkage and bulk loans and Handholding support to develop start-up and micro enterprises

- Ensuring the Institution sustainability through revenue generation

- Facilitating the backward and forward linkages for livelihood activities of urban people

- Facilitate resource mobilization through government and other agencies

- Building linkages with variety of other supporting services and resources, towards providing a wide range of services, augmenting in the process of capital, skills, employment, productive assets and infrastructure which can help overcome the multiple deprivations and risks faced by the urban poor

- CLCs managed through the CLFs function as a business incubation center for urban poor

- Good governance and professional support

Registration of CLF:

Formation of CLF:

The formation of CLF consists of minimum 5 ALFs to Maximum of 10 ALFs in corporations and 1 CLF by adjoining 2 to 3 Municipalities or Town panchayats.

So far, 78 City level Federations have been formed across the state. CLFs are mandated to submit the Annual Audit Report to the Register of Societies before September of every year for renewal.

Books of Accounts

The treasurer is the most responsible person for maintaining all the registers of CLFs besides keeping books of accounts registers. The OBs will prepare and submit all the ledgers and vouchers at the time of internal & external audit. The CLFs need to open the 4 types of accounts for different operations.

- General Fund Account: The general fund account is utilized for administrative expenditures for CLF like, salary, meeting expenses, stationery and office set up expenditures. The yearly subscription and equity fund is credited in the above account.

- Government Schemes Fund Account: The revolving fund or other Government schemes related funds are operated in this account.

- Livelihood Development fund account: The activity clusters and other livelihood related funds are operated in this account.

Business incubation center (BIS)

CLFs function in a manner similar to business incubation centres for urban poor. They

primarily focus on development of livelihood activities and EDP programs. CLFs

provide business information support, business planning and fund rising support,

provide details on eligibility of Government schemes and services which includes

common services, marketing platform and e – commerce support.

So far, 80 CLFs have been formed with 378 ALFs and 94,500 SHGs.

Philosophy of SHG Functioning

Self Help Groups (SHGs) form the primary organization of the women. SHGs have to organize and conduct their group activities strictly adhering to the in ‘Pancha Sutras’ as given below:

- Regular meetings.

- Regular savings.

- Regular internal lending.

- Regular repayments, and

- Transparent books of accounts.

- Health Hygiene & Sanitation

- Education

- Active involvement in Panchayat Raj Institutions (PRI)

- Access to entitlements & schemes

- Sustainable livelihoods

Savings and Internal Lending

Revolving Fund Support to SHGs and ALFs

The revolving fund is provided to SHGs to inculcate the habit of thrift and credit. The

revolving fund also builds institutional capacity of the SHGs in managing funds. The

revolving fund form part of the corpus along with SHG members’ own savings. The

revolving fund can also be used for internal lending. One-time Revolving Fund

support of Rs.10,000/-is provided to SHGs. ALFs are also provided with Rs 50,000

revolving fund support

So far, the TNULM disbursed the 1,26,941 SHGs with a revolving fund of Rs.127 crore in 649 ULBs

Rotation of Revolving Fund:

Revolving’ represents that the fund’s resources circulate within the group member. The intention of revolving fund providing to SHGs is to fulfill the minimum requirement of funds among the members. In TNULM, Revolving Fund is provided to SHGs which has a minimum of 70 % urban poor mobilized into the group.

So far, TNULM SHG have rotated the revolving fund to the tune of Rs 646.70 crores and 5.58 lakhs SHG members have been covering benefited 1,09,153 SHGs in urban areas.

Capacity Building of SHGs/ALFs

Capacity building of SHG members is a key prerequisite for ensuring achievement of social mobilization and poverty alleviation objectives. All SHG members are provided with 5 days of intensive training covering the following topics

- Reason for group formation

- Duties and responsibilities of the group

- Characteristics of a good group

- Financial management of the SHGs

- Rules and regulations of SHG functioning

- Planning of SHG Activities

- SHG Audit,

- Sustainability of SHG activities.

SHG Member Training:

Animator and Representative Training (A&R training):

Animator and representative training is imparted to the representatives No.1 and No.2 for two days. This training focuses on the following subjects

- Preparation and maintenance of SHG book of accounts

- Monthly reporting to District and State Mission Management Units

- Preparation and maintenance of registers for SHG Audit

- SHG Budget Preparation

- SHG Micro Credit Plan Preparation

- Training for facilitating Bank Linkages for SHGs

- Assessment of SHG loan applications

- Maintenance of loan monitoring register

- Training for Convergence with government and other institutions

A&R training is conducted by Community Resource Persons within 3 month period of SHG formation.

Under TNULM, so far 1,10,500 SHGs have been imparted A&R and Member training in 649 ULBs to the tune of 22.10 crore

Grading of SHGs/ALFs

NABARD Rating Tools of SHGs assume importance for pre-appraisal as well for self-evaluation of SHGs/ALFs. Credit Rating Index consists of two sets of variables viz. governance & systems related variables & financial variables. The Governance related parameters are frequency and regularity of meetings, attendance in the meetings, decision making methods, lending norms etc. Financial parameters include frequency & regularity of savings, use of savings, regularity of loan repayments etc. Credit Rating Index is the aggregate of the points scored on defined parameters.

Grading of SHGs is done post the completion of 3 months from formation. ALF grading is undertaken post 6 months of formation. SHGs/ALFs are graded based on parameters such as regularity of meetings, regularity of savings, internal lending to members and their repayments and maintenance of SHG/ALF books of accounts. SHG/ALF grading is undertaken by the team comprising of Community organizer, a Community resource person (CRP) and one representative from an existing ALF federation of the concerned ULB for the purpose of releasing of seed money or revolving fund.

| Marks | Grade | Grading Indicator |

|---|---|---|

| More than 90 | A+ | Excellent |

| 80 - 90 | A | Very good |

| 60 - 79 | B | Good |

| Less than 60 | C | Average |

According to the aggregate score, each group is assigned grades ‘A’, ‘B’ and ‘C’. Grade ‘A’ groups could be given loans; grade ‘B’ groups need capacity building & grade ‘C’ imply intensive capacity building is required. Thus it’s may help to assess the need of the SHGs, based on that action point may be work out for the optimum utilization of resource.

A and B graded SHGs are eligible for receiving Revolving fund (RF) or seed fund from TNULM to the tune of Rs. 10,000/- per SHG (or Rs.50,000 per ALF). This motivates the members to ensure better management and operation of the SHGs and to improve their grading to be eligible for funding. SHGs/ALFs endeavour to reach ‘A & B’ grades and to sustain the SHG movement. In the event of SHGs/ALFs obtaining C grade, refresher trainings and handholding support is provided for the next 3 months, before they become eligible for receiving the funding support.

Rating of SHGs/ALFs for Bank Linkage

Credit rating of SHGs/ALFs is undertaken in collaboration with Banking institutions in order to assess the credit worthiness of the CBOs for providing them with loans. Details are collected along two parameters viz., non-credit related information and credit related information. In the non-credit category, basic details of the applicants are taken. The credit category collects the following data to assess the credit worthiness.

- Information about existing loans – through other SHGs where the individual is a member

- Status of the SHG Account

- Name of the SHG

- SHG’s loan Account Number

- Name of the lending bank

- Amount borrowed

- Amount outstanding

- Status of the account – Regular/Defaulter/ Settled/ Sub-judice

Audit of SHGs/ALFs

District Mission Management Units and/or Area Level Federations shall be responsible for getting the books of accounts of every SHG , federated with it , audited once in year. The auditor shall audit the books of account of SHGs as per the auditing protocol and submit the report to the DMMU/ALF. On receipt of the audit report of its member SHGs, the DMMU shall pay the auditor at the rate of Rs.500/- per SHG audited by the auditor.

Based on the SHG Audit, the following outcomes are expected

- Verification of assets created by members through member’s accessed credit.

- Quality of recording of books of accounts by SHGs and individual pass books of SHG members verified. Missing / lost individual passbooks or any such gap at the member level is brought to the notice of the VO.

- Reconciliation of bank passbook and SHG books of account

- To verify if SHGs and its members have utilized the credit in the manner and purpose as enunciated in the micro credit plan

- Infuses confidence among the bankers that the SHGs are being properly monitored and regularly verified by the SHG federation.

- To come out with training needs of the SHG, which has been audited.

Thus far, 95,137 SHGs have been audited and the remaining SHGs would be audited after completion of their date of formation.

Common Interest Groups of Street Vendors

A street vendor is a person who offers goods or services for sale to the public without having a permanently built structure but with a temporary static structure or mobile stall (or head-load). Street vendors could be stationary and occupy space on the pavements or other public/private areas, or could be mobile. Lack of education and formal skill training in their respective trades/sector has rendered them vulnerable to exploitation and hence, become a subject area for intervention of the Tamil Nadu Urban Livelihoods Mission.

Financial Requirements of Street Vendor

Street vendors are a vulnerable section of the urban society, wherein they approach private money lenders for the day-to-day financial needs, towards their trading activities, at higher rates of interest. This leads to break in their continuous trading activity due to inadequate funds for business rotation and falls in the debt trap. In order to redeem them from the debt trap, timely credit at an affordable rate of interest is to be facilitated through banks. Earlier, individual street vendors were provided with individual loans provided by nationalized Banks and District Central Cooperative Banks which does not match to the growing business needs of the street vending community. The street vendors in as a group could come together with a view to contribute to the betterment of the entire vending value chain and thereby achieving economics of scale for their activities.

Hence, it is necessitated to organize the street vendors vending in a same vending zone into CIG. The banks come forward to lend them based on the business plans, comprising of individual needs and repaying capacity as a group loan, since the members are jointly liable for repayment. The banks will lend them, as cash credit loans which will be internally rotated among the members, for their day-to-day financial needs.

Urban street vendors are formed into groups by the Community Organizers with the support of the urban local body authorities and town vending committees by mobilizing the street vendors involved in vending activity in the same vending area. The business plan preparation of street vendors will be facilitated through the Community Resource Persons, Community Organizers and Assistant Project Officers (in-charge of Financial Inclusion) in the City Mission Management Unit / District Mission Management Unit.

The business plans for individual loans and group loans of street vendors are placed in the District Level Task Force headed by the District Collector and bankers and concerned department officials for approval. After approval by the District Level Task Force, the applications are sent to the concerned bank branches for sanction who in turn sanction and disburse loans based on the viability of the trades and repayment capacity.

The sanction and disbursement of loans are followed up at various levels by the Community Organizers, Assistant Project Officers, Project Director at the district level.

These concerted efforts would endorse social and economic empowerment of urban street vendors and witness the enhancement of their livelihoods.

Credit Support to CIG

- Under SEP programme of DAY – NULM the financial assistance to the urban poor street vendors in the form of interest subsidy at 7%rate of interest on bank loans for setting up individual enterprise or group enterprise may be given.

- CIG would function as one joint borrowing unit. The eligibility of CIG for group credit would depend on the combined credit requirement of all the members.

- The Financing bank would assess the credit requirement of the group, based on the nature of street vending activity and credit absorption capacity of all the members of the group. All the members would jointly execute the document and own the debt liability jointly.

- Provision of credit and other financial services of very small amounts ranging between Rs 50,000 per borrower to Rs 5,00,000 per CIG group.

- Credits can be extended to street vendors either directly or indirectly through SHG mechanism.

- To facilitate promotion of CIGs, banks are eligible for grant assistance for formation, nurturing and financing of CIG activities.

Under TNULM, So far 2511 CIGs were formed and 16,321 street vendors were covered in CIG.

SMID - Social Mobilization and Institution Development for Urban Poor

Social mobilization is the primary step of community development to organize and initiate action with their own enterprise and creativity. Through mobilization, people can organize themselves to take action collectively by developing their own plan and strategy for their socio-economic Development. TNULM envisages universal social mobilization of urban poor and vulnerable sections into Self Help Groups (SHGs) and their Federations. Generally, women from the poor and vulnerable households are mobilised as Self Help groups with a membership between 10 and 20.

TNULM lays particular emphasis on the mobilization of vulnerable sections of the urban poor population, such as SCs, STs, minorities, women-headed households, differently-abled, destitute, migrant labourers, and vulnerable occupational groups such as street vendors, rag pickers, domestic workers and construction workers etc.

Self Help Groups

Self Help Groups (SHGs) are groups of 10 to 20 women who come together to improve their living conditions by group savings and loans. These groups conduct regular meetings where the savings of the group is collected into a corpus fund, which is used to provide short-term loans to the members. After some time when the credit requirements of the members’ increase, the Self-Help Group may approach banks for loan.

As on 31st September, 2023, under TNULM, 1,38,536 SHGs have been formed in 649 ULBs and covering 15,42,487 members from Below Poverty Line HHs.

Special Self Help Groups

Organizing the vulnerable sections of the population into SHGs at the grass root level is the stepping-stone for their socio-economic development. Special Self Help Groups are being formed with differently-abled, transgenders, rag pickers or Nomadic tribes, widows, deserted women and the vulnerable people in urban areas. By networking as a group, these poor and vulnerable people can get a platform to voice their opinion and seek their entitlements. Formation of Special Self Help Groups plays an important role in inculcating the habit of creating micro savings, accessing micro loans and bank credit.

Under TNULM, so far 10,019 SHGs have been formed in 649 ULBs and covered 90,995 vulnerable members.

Categories of Special SHGs

| S.No | Types Of Special Group | No Of SHGs | No of Members Covered |

|---|---|---|---|

| 02 | Differently abled SHG | 1448 | 7964 |

| 03 | Sanitary worker SHG | 6452 | 67,746 |

| 04 | Transgender SHG | 254 | 1422 |

| 04 | Other vulnerable groups | 8723 | 69,784 |

| Total | 16,877 | 1,46,916 | |

Area Level Federations

SHGs are founding blocks for collective action. However, they can’t achieve the larger purpose of addressing poverty and aiding economic and social development due to various limitations. The major limitations include limited scope for influence, limited bargaining power, low pool of human resources and capacities, limited capability of hiring support services. SHGs are federated at various levels to achieve economies of scale, which reduces transaction costs, sharing of resources, managing partnerships, self-regulation, sustainability, and sustainable collective action. Thus, the SHG federation is an association of primary organizations uniting for perceived common benefits.

Federations in NULM are formed at Area and City Levels to strengthen SHGs and to form new SHGs, monitor SHG activities including financial, address inter-SHG issues, Area-level Health, Nutrition and Sanitation issues, Skilling at Area level, building pool of such skilled individuals for citizen referral, provide information on livelihoods, etc. and represent the area or city in various forums.

Area Level Federation (ALF) is an association of SHGs consisting of representatives from all member SHGs, with the objective of supporting member-SHGs. The federation of SHGs is essential to deal with higher-level issues like bank-linkage (including bulk loan), inter-group lending, and negotiations with higher-level structures and to gain greater bargaining power over the rights and privileges of SHGs.

Responsibilities of an ALF

- Facilitate bank linkages for member SHGs i.e. opening of their accounts and helping them getting loans.

- Providing hand-holding support in the development of loan proposals and other documentation.

- Capacity building of SHGs.

- Facilitate member SHGs’ to get the benefits under NULM as well as access to social assistance benefits under various other Government programmes.

- Support the formation of new SHGs and monitor and evaluate functioning of its member SHGs.

- Resolve issues raised by member SHGs in accessing credit from banks.

- Raise issues of importance at the level of the City-Level Federations (CLFs).

- Regularly report to the ULB about the SHG’s functioning.

Registration of ALF:

Formation of ALFs:

- Minimum 10 -20 SHGs federated to ALF in all ULBs

- Paid the prescribed admission fee and the fixed annual subscription

- Each member SHG will elect one or two of its members to represent the group in the Executive Committee of the Federation for two years term

- An Executive Committee (EC) comprise minimum 11 member elected from General body meeting with representation of member SHG

- From the EC, four members have to be selected as the Office bearers

Training to ALF - Capacity Building:

ALF Executive members have to be trained about the roles and responsibilities, Governance and Accountability, financial literacy and procedures of Societies Act and periodical refresher trainings to all Executive Committee (EC) members. TNULM is empowering the ALFs by giving training for effective functioning of ALF members are given awareness among the participants about formation of SHG federations and their role, importance of SHG federations in institution building in future course.

ALF Office Bearer Training:

ALF Executive committee member training:

The Area level federation consists of minimum 11 to maximum of 21 members based on the SHG affiliation. Each ALF has 3 Sub-committees on Financial Inclusion, Livelihood and Social security. Each sub-committee has three to five members out of which, two are selected from among the Executive Committee and three are selected from General Body. The EC members are imparted training about their roles and responsibilities in ALF EC members training programme.

Under TNULM, so far 2975 ALFs have been formed and training imparted to 9188 ALF office bearers and EC members training completed at the cost of Rs 1.74 crore

Table 1. Bulk loan received by ALFs for 2020-2021 Kadambari ALF, Arupukottai – In all table same format

So far, 2975 ALFs have been formed with 51,329 SHGs consisting of 5,90,284 SHG members. Efforts are on to federate the remaining SHGs either into existing ALFs or by forming new ALFs.

Bulk loan to ALFs:

The primary objective of the ALF is to provide financial and non-financial support to member SHGs, thereby ensuring sustainability of the SHG movement. Financial intermediation by ALF has become very essential to minimize the impact of micro finance institutions who usually charge exploitative rates of interest.

Studies undertaken by TNULM have revealed that the entire financial requirement of the SHG members, particularly seasonal and special credit requirement, are not being fully met through internal lending or SHG bank linkage. In order to bridge the gap and support its members, ALFs are encouraged to take up financial intermediary role by availing bulk loan from banks. ALF Bulk loan will result in financial empowerment of the community-based organizations which will bring in sustainability in SHG movement.

Bulk Loans to ALFs offer significant advantages such as lower transaction costs, simple documentation procedures, easier supervision, targeted credit delivery, better quality of lending and better repayment through effective peer pressure.

With the approval of Government of Tamil Nadu, ALFs have been empowered to avail loan from Banks and lend to SHGs for gap filling required for financing and safe guard them from falling prey under the clutches of money lenders and other costly loan options for their short-term loans/ working capital requirements at an exorbitant interest rate.

For financial year, 2021-22 the various banks have lent bulk loan to 6 ALFs to the tune of Rs.1.96 crore. The ALFs facilitated the micro enterprises run by ALFs/ SHGs and motivate them to undertake profitable economic activities. Despite the fact that ALFs availing bulk loans are not eligible to receive Interest Subvention from DAY-NULM scheme, the District Mission Management Units in Tamil Nadu have always strived to set an example to the nation in facilitating higher levels of credit linkage through bulk loans in urban areas. The state Mission has also written to the National Mission to consider release of Interest subvention to ALFs availing Bulk Loans.

Table 1. Bulk loan received by ALFs for 2020-2021

| S.No | Name of the District | Name of the ALF | Amount of Bulk loan (Rs .Lakhs) | No of SHG benefited | No of LH activities supported through Bulk loan |

|---|---|---|---|---|---|

| 1 | Cuddalore | Malumiyarpettai ALF | 42 | 12 | 100 |

| 2 | Virudhungar | Kadambari ALF. Arupukottai | 16.69 | 9 | 114 |

| Adharsana ALF Chettiarpatty | 20.00 | 10 | 112 | ||

| 3 | Madurai | Pothugai ALF ,Balamedu | 39.05 | 9 | 92 |

| Karmugil ALF, Paravai | 19.05 | 4 | 46 | ||

| 4 | Tirunelveli | Jansi Rani ALF | 60 | 6 | 70 |

| Total | 196.79 | 50 | 534 | ||

Thus far, 2975 ALFs have been formed with 51,329 SHGs and consisting of 5,90,284 SHG members. Efforts are on to federate the remaining SHGs either into existing ALFs or by forming newer ALFs.

City Level Federations

- Strengthening of CBOs like SHGs, ALF and CLC in urban area

- Capacity building of CBOs about the scheme’s sensitization, awareness creation and capacity building training

- Resource mobilization and revenue generation for institutional sustenance and sustainability

- Facilitate the livelihood promotion through CBOs like, SHGs ALF and CLC through Bank Linkage and bulk loans and Handholding support to develop start-up and micro enterprises

- Ensuring the Institution sustainability through revenue generation

- Facilitating the backward and forward linkages for livelihood activities of urban people

- Facilitate resource mobilization through government and other agencies

- Building linkages with variety of other supporting services and resources, towards providing a wide range of services, augmenting in the process of capital, skills, employment, productive assets and infrastructure which can help overcome the multiple deprivations and risks faced by the urban poor

- CLCs managed through the CLFs function as a business incubation center for urban poor

- Good governance and professional support

Registration of CLF:

Formation of CLF:

The formation of CLF consists of minimum 5 ALFs to Maximum of 10 ALFs in corporations and 1 CLF by adjoining 2 to 3 Municipalities or Town panchayats.

So far, 78 City level Federations have been formed across the state. CLFs are mandated to submit the Annual Audit Report to the Register of Societies before September of every year for renewal.

Books of Accounts

The treasurer is the most responsible person for maintaining all the registers of CLFs besides keeping books of accounts registers. The OBs will prepare and submit all the ledgers and vouchers at the time of internal & external audit. The CLFs need to open the 4 types of accounts for different operations.

- General Fund Account: The general fund account is utilized for administrative expenditures for CLF like, salary, meeting expenses, stationery and office set up expenditures. The yearly subscription and equity fund is credited in the above account.

- Government Schemes Fund Account: The revolving fund or other Government schemes related funds are operated in this account.

- Livelihood Development fund account: The activity clusters and other livelihood related funds are operated in this account.

Business incubation center (BIS)

CLFs function in a manner similar to business incubation centres for urban poor. They

primarily focus on development of livelihood activities and EDP programs. CLFs

provide business information support, business planning and fund rising support,

provide details on eligibility of Government schemes and services which includes

common services, marketing platform and e – commerce support.

So far, 80 CLFs have been formed with 378 ALFs and 94,500 SHGs.

Philosophy of SHG Functioning

Self Help Groups (SHGs) form the primary organization of the women. SHGs have to organize and conduct their group activities strictly adhering to the in ‘Pancha Sutras’ as given below:

- Regular meetings.

- Regular savings.

- Regular internal lending.

- Regular repayments, and

- Transparent books of accounts.

- Health Hygiene & Sanitation

- Education

- Active involvement in Panchayat Raj Institutions (PRI)

- Access to entitlements & schemes

- Sustainable livelihoods

Savings and Internal Lending

Revolving Fund Support to SHGs and ALFs

The revolving fund is provided to SHGs to inculcate the habit of thrift and credit. The

revolving fund also builds institutional capacity of the SHGs in managing funds. The

revolving fund form part of the corpus along with SHG members’ own savings. The

revolving fund can also be used for internal lending. One-time Revolving Fund

support of Rs.10,000/-is provided to SHGs. ALFs are also provided with Rs 50,000

revolving fund support

So far, the TNULM disbursed the 1,26,941 SHGs with a revolving fund of Rs.127 crore in 649 ULBs

Rotation of Revolving Fund:

Revolving’ represents that the fund’s resources circulate within the group member. The intention of revolving fund providing to SHGs is to fulfill the minimum requirement of funds among the members. In TNULM, Revolving Fund is provided to SHGs which has a minimum of 70 % urban poor mobilized into the group.

So far, TNULM SHG have rotated the revolving fund to the tune of Rs 646.70 crores and 5.58 lakhs SHG members have been covering benefited 1,09,153 SHGs in urban areas.

Capacity Building of SHGs/ALFs

Capacity building of SHG members is a key prerequisite for ensuring achievement of social mobilization and poverty alleviation objectives. All SHG members are provided with 5 days of intensive training covering the following topics

- Reason for group formation

- Duties and responsibilities of the group

- Characteristics of a good group

- Financial management of the SHGs

- Rules and regulations of SHG functioning

- Planning of SHG Activities

- SHG Audit,

- Sustainability of SHG activities.

SHG Member Training:

Animator and Representative Training (A&R training):

Animator and representative training is imparted to the representatives No.1 and No.2 for two days. This training focuses on the following subjects

- Preparation and maintenance of SHG book of accounts

- Monthly reporting to District and State Mission Management Units

- Preparation and maintenance of registers for SHG Audit

- SHG Budget Preparation

- SHG Micro Credit Plan Preparation

- Training for facilitating Bank Linkages for SHGs

- Assessment of SHG loan applications

- Maintenance of loan monitoring register

- Training for Convergence with government and other institutions

A&R training is conducted by Community Resource Persons within 3 month period of SHG formation.

Under TNULM, so far 1,10,500 SHGs have been imparted A&R and Member training in 649 ULBs to the tune of 22.10 crore

Grading of SHGs/ALFs

NABARD Rating Tools of SHGs assume importance for pre-appraisal as well for self-evaluation of SHGs/ALFs. Credit Rating Index consists of two sets of variables viz. governance & systems related variables & financial variables. The Governance related parameters are frequency and regularity of meetings, attendance in the meetings, decision making methods, lending norms etc. Financial parameters include frequency & regularity of savings, use of savings, regularity of loan repayments etc. Credit Rating Index is the aggregate of the points scored on defined parameters.

Grading of SHGs is done post the completion of 3 months from formation. ALF grading is undertaken post 6 months of formation. SHGs/ALFs are graded based on parameters such as regularity of meetings, regularity of savings, internal lending to members and their repayments and maintenance of SHG/ALF books of accounts. SHG/ALF grading is undertaken by the team comprising of Community organizer, a Community resource person (CRP) and one representative from an existing ALF federation of the concerned ULB for the purpose of releasing of seed money or revolving fund.

| Marks | Grade | Grading Indicator |

|---|---|---|

| More than 90 | A+ | Excellent |

| 80 - 90 | A | Very good |

| 60 - 79 | B | Good |

| Less than 60 | C | Average |

According to the aggregate score, each group is assigned grades ‘A’, ‘B’ and ‘C’. Grade ‘A’ groups could be given loans; grade ‘B’ groups need capacity building & grade ‘C’ imply intensive capacity building is required. Thus it’s may help to assess the need of the SHGs, based on that action point may be work out for the optimum utilization of resource.

A and B graded SHGs are eligible for receiving Revolving fund (RF) or seed fund from TNULM to the tune of Rs. 10,000/- per SHG (or Rs.50,000 per ALF). This motivates the members to ensure better management and operation of the SHGs and to improve their grading to be eligible for funding. SHGs/ALFs endeavour to reach ‘A & B’ grades and to sustain the SHG movement. In the event of SHGs/ALFs obtaining C grade, refresher trainings and handholding support is provided for the next 3 months, before they become eligible for receiving the funding support.

Rating of SHGs/ALFs for Bank Linkage

Credit rating of SHGs/ALFs is undertaken in collaboration with Banking institutions in order to assess the credit worthiness of the CBOs for providing them with loans. Details are collected along two parameters viz., non-credit related information and credit related information. In the non-credit category, basic details of the applicants are taken. The credit category collects the following data to assess the credit worthiness.

- Information about existing loans – through other SHGs where the individual is a member

- Status of the SHG Account

- Name of the SHG

- SHG’s loan Account Number

- Name of the lending bank

- Amount borrowed

- Amount outstanding

- Status of the account – Regular/Defaulter/ Settled/ Sub-judice

Audit of SHGs/ALFs

District Mission Management Units and/or Area Level Federations shall be responsible for getting the books of accounts of every SHG , federated with it , audited once in year. The auditor shall audit the books of account of SHGs as per the auditing protocol and submit the report to the DMMU/ALF. On receipt of the audit report of its member SHGs, the DMMU shall pay the auditor at the rate of Rs.500/- per SHG audited by the auditor.

Based on the SHG Audit, the following outcomes are expected

- Verification of assets created by members through member’s accessed credit.

- Quality of recording of books of accounts by SHGs and individual pass books of SHG members verified. Missing / lost individual passbooks or any such gap at the member level is brought to the notice of the VO.

- Reconciliation of bank passbook and SHG books of account

- To verify if SHGs and its members have utilized the credit in the manner and purpose as enunciated in the micro credit plan

- Infuses confidence among the bankers that the SHGs are being properly monitored and regularly verified by the SHG federation.

- To come out with training needs of the SHG, which has been audited.

Thus far, 95,137 SHGs have been audited and the remaining SHGs would be audited after completion of their date of formation.

Common Interest Groups of Street Vendors

A street vendor is a person who offers goods or services for sale to the public without having a permanently built structure but with a temporary static structure or mobile stall (or head-load). Street vendors could be stationary and occupy space on the pavements or other public/private areas, or could be mobile. Lack of education and formal skill training in their respective trades/sector has rendered them vulnerable to exploitation and hence, become a subject area for intervention of the Tamil Nadu Urban Livelihoods Mission.

Financial Requirements of Street Vendor

Street vendors are a vulnerable section of the urban society, wherein they approach private money lenders for the day-to-day financial needs, towards their trading activities, at higher rates of interest. This leads to break in their continuous trading activity due to inadequate funds for business rotation and falls in the debt trap. In order to redeem them from the debt trap, timely credit at an affordable rate of interest is to be facilitated through banks. Earlier, individual street vendors were provided with individual loans provided by nationalized Banks and District Central Cooperative Banks which does not match to the growing business needs of the street vending community. The street vendors in as a group could come together with a view to contribute to the betterment of the entire vending value chain and thereby achieving economics of scale for their activities.

Hence, it is necessitated to organize the street vendors vending in a same vending zone into CIG. The banks come forward to lend them based on the business plans, comprising of individual needs and repaying capacity as a group loan, since the members are jointly liable for repayment. The banks will lend them, as cash credit loans which will be internally rotated among the members, for their day-to-day financial needs.

Urban street vendors are formed into groups by the Community Organizers with the support of the urban local body authorities and town vending committees by mobilizing the street vendors involved in vending activity in the same vending area. The business plan preparation of street vendors will be facilitated through the Community Resource Persons, Community Organizers and Assistant Project Officers (in-charge of Financial Inclusion) in the City Mission Management Unit / District Mission Management Unit.

The business plans for individual loans and group loans of street vendors are placed in the District Level Task Force headed by the District Collector and bankers and concerned department officials for approval. After approval by the District Level Task Force, the applications are sent to the concerned bank branches for sanction who in turn sanction and disburse loans based on the viability of the trades and repayment capacity.

The sanction and disbursement of loans are followed up at various levels by the Community Organizers, Assistant Project Officers, Project Director at the district level.

These concerted efforts would endorse social and economic empowerment of urban street vendors and witness the enhancement of their livelihoods.

Credit Support to CIG

- Under SEP programme of DAY – NULM the financial assistance to the urban poor street vendors in the form of interest subsidy at 7%rate of interest on bank loans for setting up individual enterprise or group enterprise may be given.

- CIG would function as one joint borrowing unit. The eligibility of CIG for group credit would depend on the combined credit requirement of all the members.

- The Financing bank would assess the credit requirement of the group, based on the nature of street vending activity and credit absorption capacity of all the members of the group. All the members would jointly execute the document and own the debt liability jointly.

- Provision of credit and other financial services of very small amounts ranging between Rs 50,000 per borrower to Rs 5,00,000 per CIG group.

- Credits can be extended to street vendors either directly or indirectly through SHG mechanism.

- To facilitate promotion of CIGs, banks are eligible for grant assistance for formation, nurturing and financing of CIG activities.

Under TNULM, So far 2511 CIGs were formed and 16,321 street vendors were covered in CIG.